ACES’ Mortgage QC Industry Trends Report represents an analysis of nationwide quality control findings based on data derived from the ACES Quality Management & Control Software.

Executive Summary

QC Industry Trends – Overview

QC Industry Trends – by Category

QC Industry Trends – by Loan Purpose

QC Industry Trends – by Loan Type

Early Payment Defaults

Conclusion

About this Report

Executive Summary

This report represents an analysis of post-closing quality control data derived from loan files analyzed by the ACES Quality Management and Control® benchmarking system during the third quarter of 2020 (Q3 2020) and incorporates data from prior quarters and/or calendar years, where applicable.

Findings for the Q3 2020 Trends Report were based on post-closing quality control data from approximately 100,000 unique records. All reviews and defect data that were evaluated for this report were based on loan audits selected by lenders for full file reviews.

Defects are categorized using the Fannie Mae loan defect taxonomy. Data analysis for any given quarter does not begin until 90-days after the end of the quarter to allow lenders to complete the post-closing quality control cycle, resulting in a delay between the end of the quarter and publication of the data.

NOTE: A critical defect is defined as a defect that would result in the loan being uninsurable or ineligible for sale. The critical defect rate reflects the percentage of loans reviewed for which at least one critical defect was identified during the post-closing quality control review, and all reported defects are net defects.

Summary of Findings

There is no way to sugarcoat it – Q3 was a volatile quarter for loan quality. COVID continued to wreak havoc on the economy, and lenders struggled with volume increases, COVID-related compliance changes, and continued high unemployment numbers. In this report, we will talk about those factors as well as the interest rate environment and other macro-economic factors that provide insight into the critical defect rate.

Report highlights include the following findings:

- The overall critical defect rate of 2.34% represents a marked increase from prior quarters and is the highest observed since ACES began publishing the QC Trends Report in 2016.

- While rates remained low, Q3 also brought newsworthy events that may have impacted performance.

- Income/Employment defect share fell – a positive sign – but manufacturing-related defects grew.

- Record lending volume combined with summer home buying led to an increase in overall purchase share from the prior quarter.

- Conventional loans had a strong market share, but quality slipped a bit in Q3.

- There is reason to be cautiously optimistic on Early Payment Defaults (EPD).

QC Industry Trends – Overview

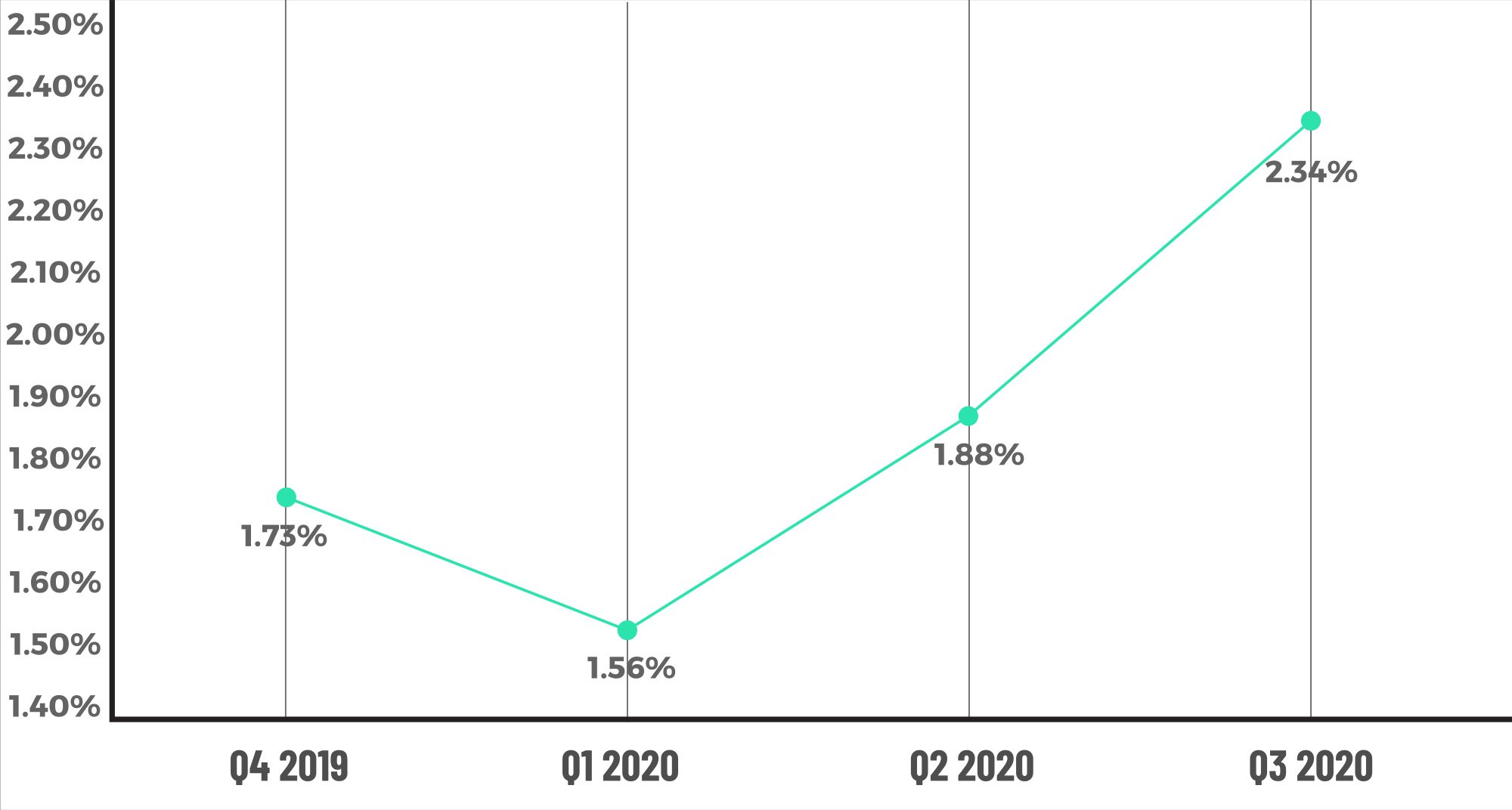

The overall critical defect rose to 2.34% in Q3 2020, up 25% from Q2’s 1.88%. The recent trend is clearly in the wrong direction, with the defect rate having increased in three of the prior five quarters. It can be difficult to pinpoint with absolute certainty why the defect rate would rise, though this report examines several possible factors.

In trying to make sense of changes to the defect rate, ACES typically looks first to the economy and regulatory or other major impacts to the mortgage industry. We believe the prior quarter’s (Q2 2020) rise in defect rates was partially driven by the dramatic spike in unemployment in such a short period of time. According to official unemployment statistics put out by the Bureau of Labor Statistics, unemployment rates peaked in April at roughly 15% and had declined to just over 10% at the beginning of Q3 20201. That same rate declined further during the quarter to just under 8%. While still more than double the 4% unemployment rate prior to the pandemic, the number would seem to indicate that the overall health of borrowers improved during Q3 2020. The unemployment data can be nuanced, however, and remember that it represents only those citizens, of working age, that are unemployed but still part of the labor force (i.e. they are looking for work). In the pandemic, it has been difficult to tell how many people have left the labor force, and it is estimated that the number of those that have left is elevated because they are caring for sick relatives, do not have childcare due to the pandemic, or other reasons.

Interest rates obviously play a key role in the data as well. Like unemployment rates, interest rates signaled good news, at least as they affect the mortgage market. According to Freddie Mac’s Primary Mortgage Market Survey® data2, the average rate on a 30-year fixed rate stood at 3.07% in July 2020, the start of Q3. That same rate was 2.88% by the end of the quarter. Rates drove refinance volumes and propelled Q3 2020 to the largest quarter of mortgage originations in 13 years. Lenders originated 3.25 million residential mortgages in Q3 2020, up 17% from the prior quarter and 45% from the same quarter in 2019, according to Attom Data Solutions3. Increases in the critical defect rate in periods of rapidly rising volumes are not uncommon, though they are often temporary as lenders adjust staffing and processes to meet the volume challenges. This is something that ACES will be watching closely in the coming quarters.

There was also a major disruptive event in Q3 2020, and that was the August 13th announcement by FHFA of an “adverse market refinance fee” of 0.5%. The fee was originally scheduled to go into effect in September. Because of the short lead time, lenders had a frenetic couple of weeks figuring out what to do on loans that were already locked but not able to be originated and delivered to the agencies prior to the effective date. The fee was later deferred to December 1st and it is difficult to say what effect the announcement alone had on defect rates. We do know that lenders’ manufacturing process was chaotic for a couple of weeks as a result.

1. https://www.bls.gov/news.release/pdf/empsit.pdf

2. http://www.freddiemac.com/pmms/

3. https://www.attomdata.com/news/market-trends/mortgage-origination/attom-data-solutions-q3-2020-u-s-residential-property-mortgage-origination-report/

Critical Defect Rate by Quarter: Q4 2019 – Q3 2020

Figure 1 displays the percentage of loans with critical defects by quarter, Q4 2019 through Q3 2020.

QC Industry Trends by Defect Category

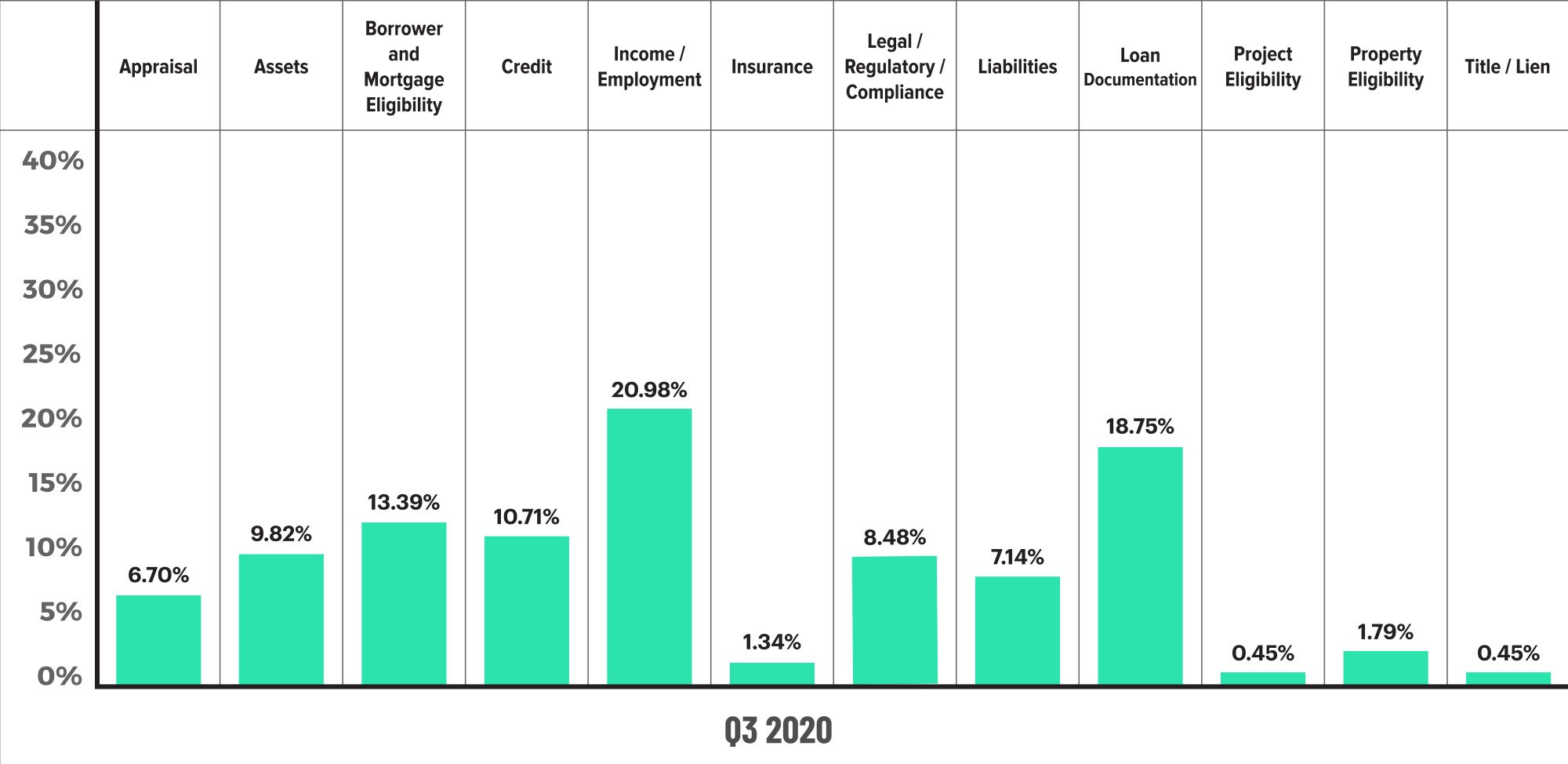

The defect news was not all bad in Q3 2020. Defects attributed to Income/ Employment fell 9 points to 21% in Q3 2020, which falls in line with the improvement in unemployment numbers. Of the Big Four categories that ACES monitors closely (Income, Assets, Credit, and Liabilities), three saw their share of defects decline in Q3 2020 as compared to the prior quarter. These categories include: Assets (10%, down from 12+%), Credit (11%, down from 19%), and Income (21%, down from 30%). Of the Big Four, only the Liabilities category gained in defect share, with a 4-point increase to 7% in Q3 2020 – up from 3% in the prior quarter. ACES believes that future defect rate moderation will be led by decreases in the Big Four categories, which are primary indicators of borrower health.

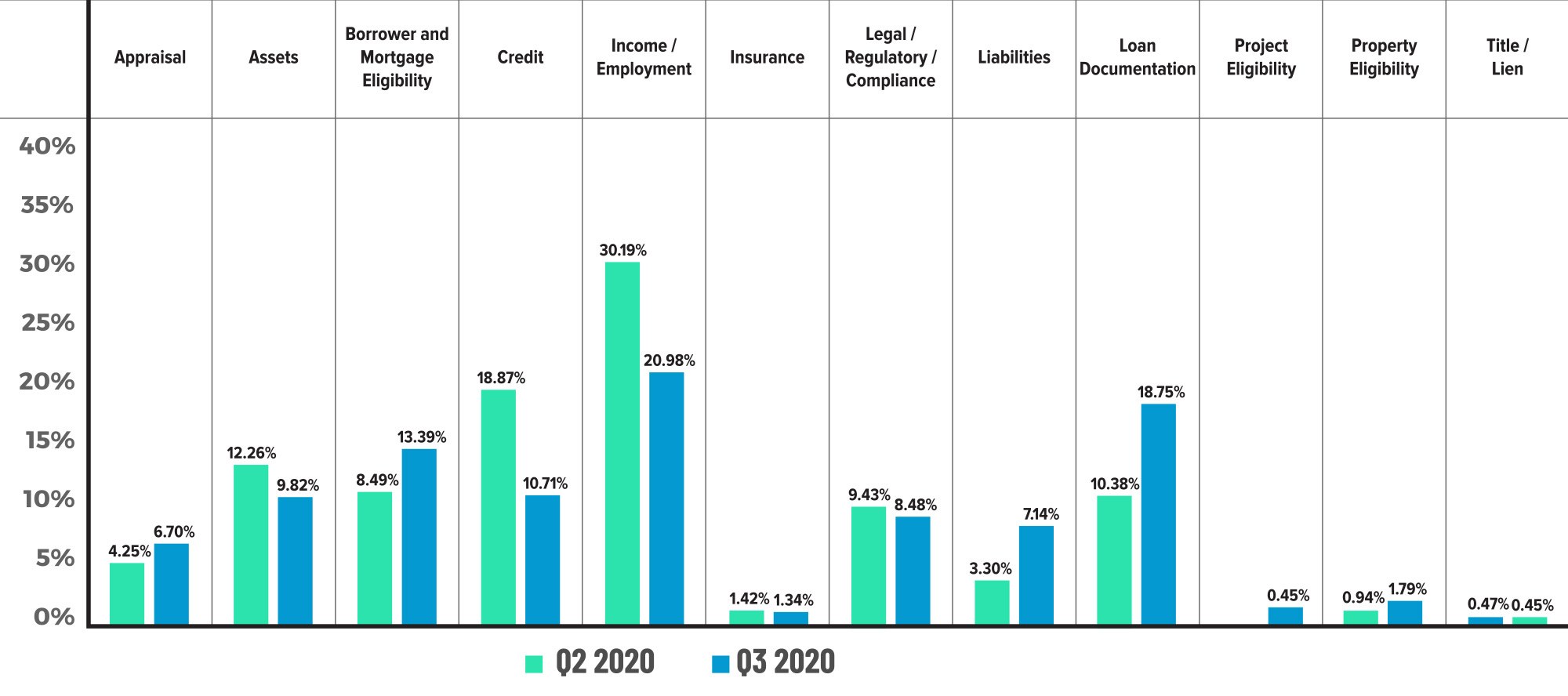

In Figure 3, trending shows five of the defect categories saw a rise in defect share, while five saw a decline and one remained roughly the same as the prior quarter. Of the categories that increased, none of the increases were large enough to cause alarm. The largest increases were in the manufacturing-related categories of Loan Documentation (+8.5% this quarter compared to last quarter) and Borrower/Mortgage Eligibility (+5%). Appraisal defects are one category to keep an eye on, as those defects rose nearly 3 points from the previous quarter to almost 7% in Q3 2020. A hopeful sign for future quarters was evident in the Income and Credit categories which saw the steepest declines.

Critical Defects by Fannie Mae Category: Q3 2020

Figure 2 displays the dispersion of critical defects across Fannie Mae categories for Q3 2020.

Critical Defects by Fannie Mae Category: Q2 2020 vs. Q3 2020

Figure 3 displays the critical defect rate by Fannie Mae category comparing Q2 2020 to Q3 2020.

QC Industry Trends by Loan Purpose

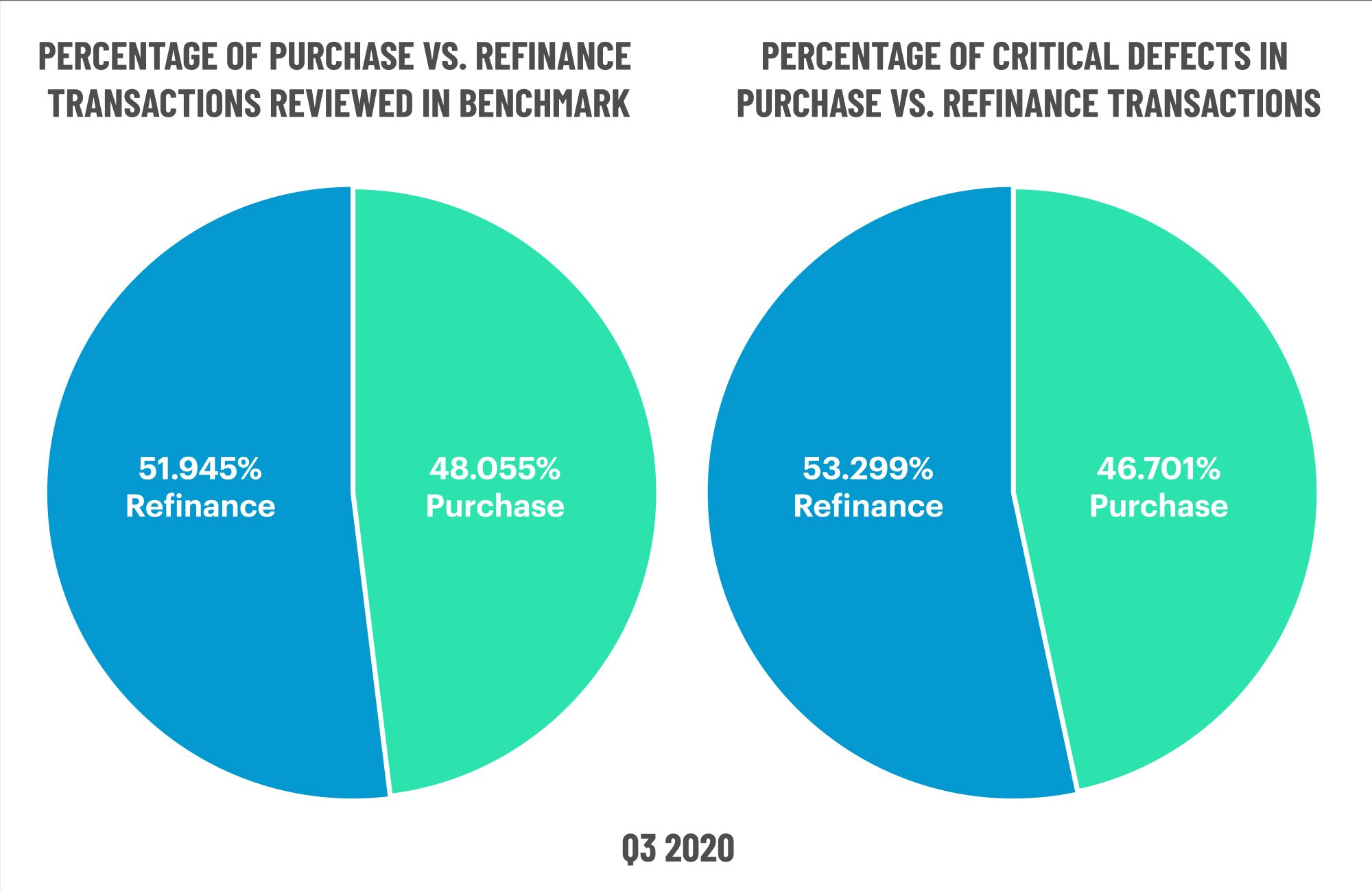

As mentioned earlier, residential mortgage lending volumes in Q3 2020 were the highest in more than a decade. ACES’ data shows a surge in both purchases and refinances in terms of overall volume. However, the share of purchases picked up steam in the typical seasonal buying period of July through September, and the share of each was roughly equal. Purchases comprised 48% of the loans reviewed, and refinances ended the quarter at 52%. In the prior quarter, refinances held a 56% share and purchases were 44%. These trends still indicate a refinance-dominated market, and as recently as CY 2019, refinance share was 35%. Interest rates remained low throughout the end of 2020, hitting all-time lows in both Q3 and Q4. This trend is expected to continue through Q1 of 2021. It will be interesting to see what impact the FHFA’s adverse market refinance fee has on the refinance and purchase share numbers after it took effect on December 1st, 2020.

Defect performance did change slightly in Q3 2020. For the prior two quarters, ACES observed defect parity, in which both the loan share and defect share were equal. In Q3, refinances made up 52% of loans reviewed but accounted for over 53% of overall defects. Conversely, purchase transactions comprised 48% of the loans reviewed and made up just under 47% of the defects. These numbers indicate a slight degradation in refinance performance. Looking at these numbers in the context of the defects by category, the increase manufacturing-related problems has a direct correlation to underperformance issues in refinances. Lenders typically mobilize quickly to correct these issues, and ACES will be monitoring these items in future quarters.

Figure 4 displays the loans reviewed and critical defects by loan type for Q3 2020.

QC Industry Trends by Loan Type

We continue to see strong share performance for conventional loans. In Q3 2020, conventional share saw a 1.5% increase, totaling 72%. The share of FHA loans also increased by a point from the prior quarter reaching 19% in Q3. Both of these increases came at the expense of VA lending, which fell to 6% in Q3 2020 from 8% in the prior quarter.

Looking at a slightly longer timeframe, these trends show a steady decline in FHA share. In CY 2018, FHA held a 31% share which was slightly higher compared to CY 2019 when it was just over 27%. Conventional share benefits over the same time horizon, increasing from 56% in CY 2018 to 62% in CY 2019, and is on pace to pick up 10% within the next year and almost 20% over a two-year period.

However, the data is not as kind to conventional loans when looking at defect share. Typically, the percentage of defects attributed to conventional loans is less than its share of total loans reviewed. Although conventional loans made up 72% of the loans reviewed for Q3, they made up 75% of the defects. By comparison, conventional loans had a 71% share last quarter and only made up 67% of the defects. For CY 2019, this spread was even larger with a 62% share and 49% of defects. Clearly, there is an upward trend in defects in conventional loans, even as their share continues to climb. If there is a silver lining, it is that FHA performance is improving. This quarter FHA achieved defect parity, with both a 19% share of loans and share of defects.

Figure 5 displays the loans reviewed and critical defects by loan type for Q3 2020.

Early Payment Defaults

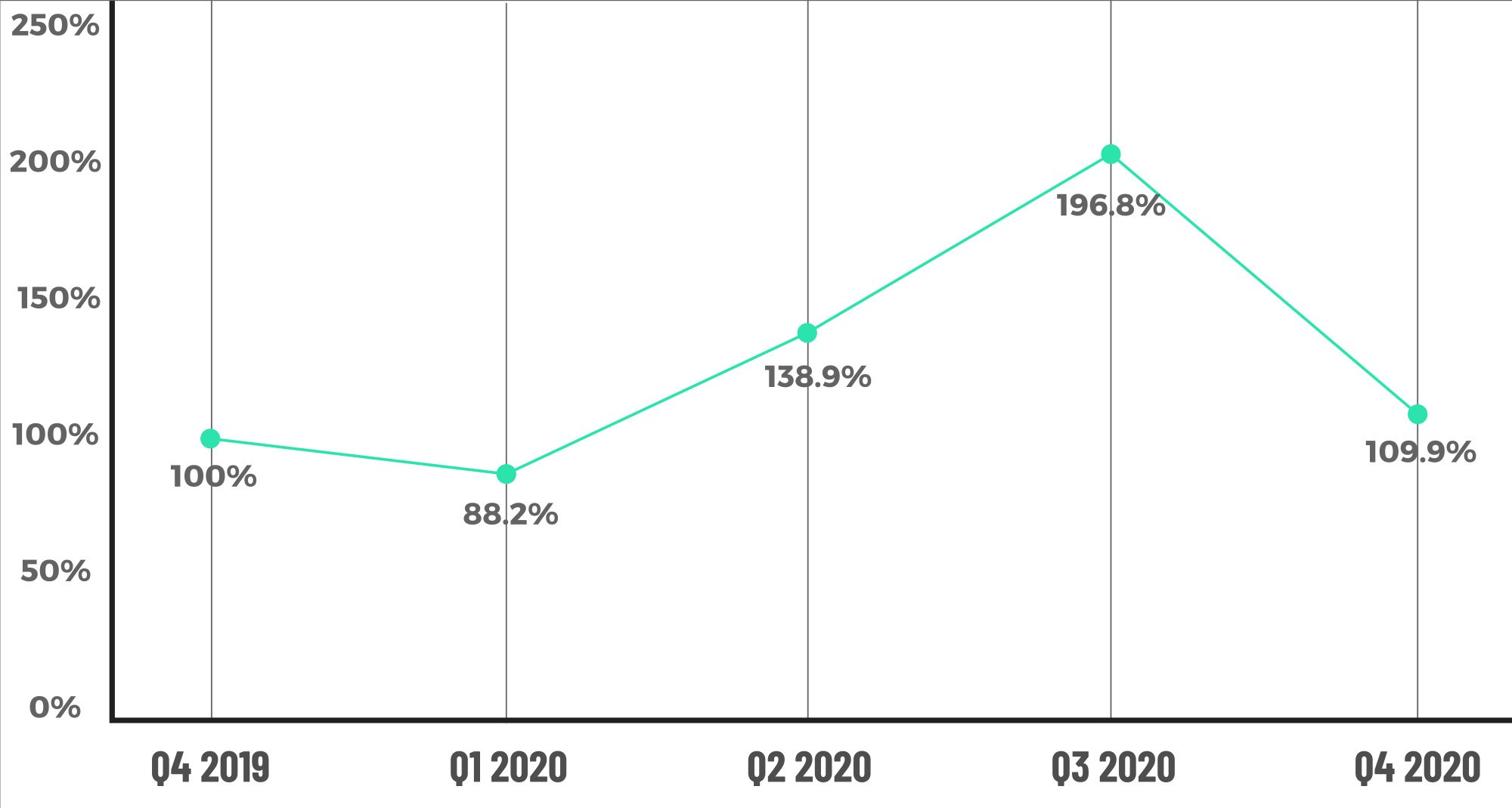

Early Payment Default (EPD) data is in for all of 2020, and in the most recent quarter (Q4), we saw some positive signs. After a 200% increase in Q3 2020, the number of EPD reviews processed through ACES in Q4 2020 declined to just 110% of the pre-pandemic benchmark, putting it just 10% over Q4 2019’s numbers. Because EPD lookback periods can last up to a year, lenders are not out of the woods yet, but these numbers are encour- aging after experiencing three straight quarters of increases.

The question now becomes whether EPDs reached their peak in Q3 2020 and if the industry will see a reversion to the mean going forward. ACES will release January 2021 EPD data during our upcoming QC Now webinar in May 2021.

Early Payment Default Percentage by Quarter: Q4 2019 – Q4 2020

Figure 6 displays the EPD % by quarter from Q4 2019 to Q4 2020.

Conclusion

The critical defect data for Q3 2020 is discouraging after nearly two straight years of good performance. This quarter had several impactful and newsworthy events that most likely played some part in the decline in performance, including the “adverse market fee” in August and the expiration of some of the original CARES Act stimulus. Additionally, the political back-and-forth to extend some of the more popular features of the CARES Act, such as unemployment extension and direct payments to eligible Americans, also had an impact on the market, with Congress ultimately passing CARES Act II in December. All of these factors contributed to this quarter’s defect rates, though some more directly than others. Due to all of these factors and more, ACES expects continued volatility in defect rates for at least several more quarters.

One sign that is not directly related to defect rates but signals the overall health of the economy is the ability of lenders to raise equity in the capital markets. A number of lenders converted to publicly-traded companies in the second half of 2020 and into early 2021. Institutional and retail investors have put their faith in the mortgage market’s ability to grow and be a reliable place in which to invest. SEC filing requirements have also made information that was historically very closely held more accessible to the public, thus disclosing that lenders were extremely profitable in Q2 and Q3. This resulted in some of the publicly-traded lenders reporting 5+% gain-on-sale numbers in Q2 and most maintaining above 4% in Q3. Keep in mind that Q3 was the largest volume of originations in more than a decade, so that volume was highly profitable.

Looking to Q4 and beyond, ACES will be watching to see if the defects can outperform Q3. With continued low interest rates and the end of the summer buying season, we expect the see similar strong shares of refinances and conventional loans. In addition, there is the actual implementation of the adverse market fee with which to contend, and not to foreshadow too much, but interest rates did jump unexpectedly in Q1 2021. The industry has been through this before, most recently the end of 2018, and it is important to remember that cycles in the mortgage industry are normal and somewhat unavoidable, and as such, lenders need to keep their eyes on the trends to measure quality improvement and degradation. In the end, the raw numbers do matter, but context is also equally important.

About the ACES Mortgage QC Industry Trends Report

The ACES Mortgage QC Industry Trends Report represents a nationwide post-closing quality control analysis using data and findings derived from mortgage lenders utilizing the ACES Analytics benchmarking software.

This report provides an in-depth analysis of residential mortgage critical defects as re- ported during post-closing quality control audits. Data presented comprises net critical defects and is categorized in accordance with the Fannie Mae loan defect taxonomy.

About ACES

ACES Quality Management, formerly known as ACES Risk Management (ARMCO), is the leading provider of enterprise quality management and control software for the financial services industry. The nation’s most prominent lenders, servicers and financial institutions rely on ACES Quality Management & Control® Software to improve audit throughput and quality while controlling costs, including:

- 3 of the top 5 and more than 50% of the top 50 independent mortgage lenders;

- 7 of the top 10 loan servicers;

- 11 of the top 30 banks; and

- 1 of the top 3 credit unions in the USA.

Unlike other quality control platforms, only ACES delivers Flexible Audit Technology, which gives independent mortgage lenders and financial institutions the ability to easily manage and customize ACES to meet their business needs without having to rely on IT or other outside resources. Using a customer-centric approach, ACES clients get responsive support and access to our experts to maximize their investment.

For more information, visit www.acesquality.com or call 1-800-858-1598.

Media Contact: Lindsey Neal | DepthPR for ACES | (404) 549-9282 | lindsey@depthpr.com

View all reports